“So that the record of history is absolutely crystal clear that there is no alternative way, so far discovered, of improving the lot of the ordinary people that can hold a candle to the productive activities that are unleashed by a free enterprise system.”

- Milton Friedman,

Nobel Prize-Winning Economist

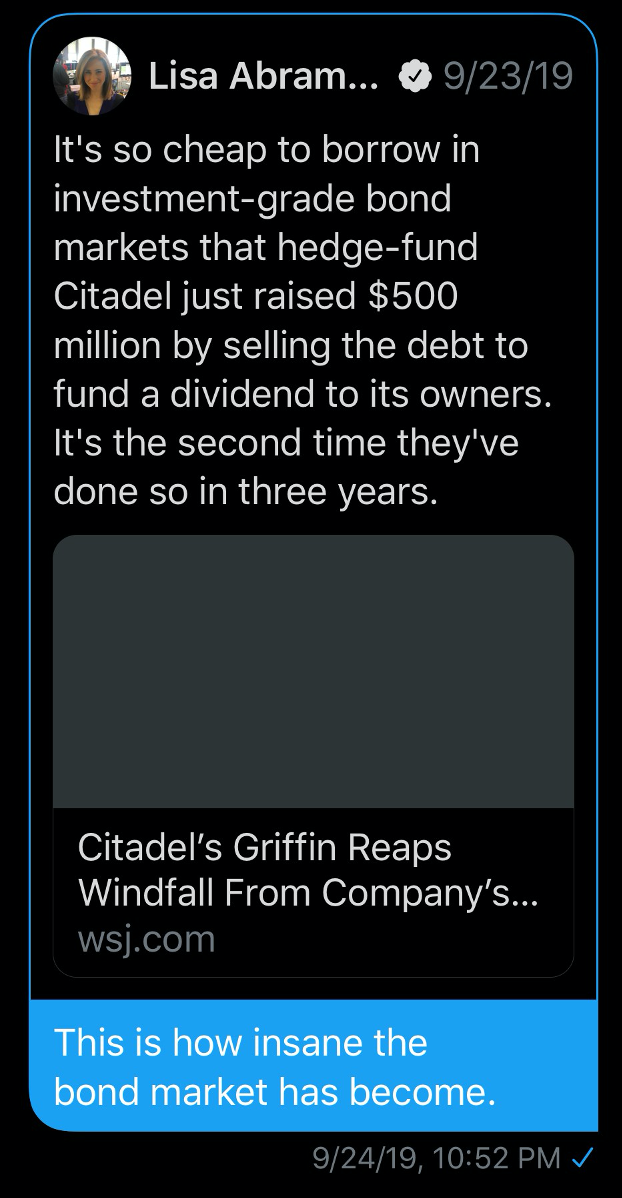

I was speechless, angry. Yesterday (April 9, 2020), across the tape scrolled the news: “The Fed to buy high-yield junk bonds and lend to states.” Twitter lit up. Emails came flooding in. One of the best came from my friend Chris Hempstead. It was titled, “The Fed has WOKE the market.... again!”

I called Chris and he summed it up in one sentence, “We are playing a video game that doesn’t require quarters—nobody loses in this game.” No money required. No risk of failure. Just press the button and a new game loads.

Two weeks ago, I shared with you a Bloomberg article written by Camp Kotok fishing friend Jim Bianco. The title: “The Fed’s Cure Risks Being Worse Than the Disease.” From Jim:

"An alphabet soup of new asset-buying programs will essentially nationalize large swaths of the financial markets, and the consequences could be profound.

The economic debate of the day centers on whether the cure of an economic shutdown is worse than the disease of the virus. Similarly, we need to ask if the cure of the Federal Reserve getting so deeply into corporate bonds, asset-backed securities, commercial paper, and exchange-traded funds is worse than the disease seizing financial markets. It may be."

Wondering how we get back to that “press start” screen without a single quarter?

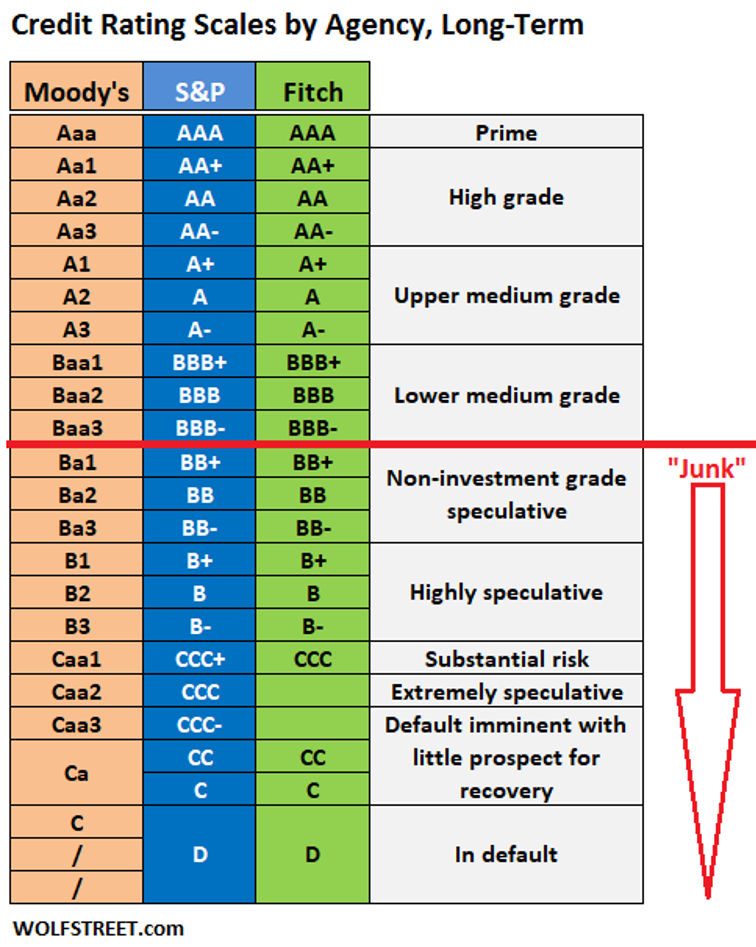

The Fed creates a special purpose vehicle, or SPV. The Fed prints money and buys bonds from the Treasury. The Treasury takes that money and puts in into the SPV. The Fed then uses the money in the SPV to do stuff like buy high-yield junk bonds. A fire starts somewhere, create an SPV. New fire, new SPV.

Again, from Jim:

"But it’s the alphabet soup of new programs that deserve special consideration, as they could have profound long-term consequences for the functioning of the Fed and the allocation of capital in financial markets.

To put it bluntly, the Fed isn’t allowed to do any of this. The central bank is only allowed to purchase or lend against securities that have government guarantee. This includes Treasury securities, agency mortgage-backed securities and the debt issued by Fannie Mae and Freddie Mac. An argument can be made that can also include municipal securities, but nothing in the laundry list above.

So how can they do this? The Fed will finance a special purpose vehicle (SPV) for each acronym to conduct these operations. The Treasury, using the Exchange Stabilization Fund, will make an equity investment in each SPV and be in a “first loss” position. What does this mean? In essence, the Treasury, not the Fed, is buying all these securities and backstopping of loans; the Fed is acting as banker and providing financing. The Fed hired BlackRock Inc. to purchase these securities and handle the administration of the SPVs on behalf of the owner, the Treasury.

In other words, the federal government is nationalizing large swaths of the financial markets. The Fed is providing the money to do it. BlackRock will be doing the trades."

Jim concluded, “This scheme essentially merges the Fed and Treasury into one organization. So, meet your new Fed chairman, Donald J. Trump.”

And the next president, and the next. When I arrived home last evening, my wife, Susan, knew I was off. She said, “This is what you’ve been saying is coming.” True, but it deeply troubles me. We are entering a dark cave with a dimly lit flashlight. I’m not sure how we make our way to the other side. I’m putting some red wine in my backpack.

Chris Hempstead is one of the good guys. He’s been in the game for years. He was a specialist on the American Stock Exchange trading QQQs for 20 years, working for one of the major players—a firm called Susquehanna International Group. When electronic trading took hold, like most floor brokers, he moved to trading desk at WallachBeth and later Deutsche Bank. Today, he’s the Director of Institutional Business Development at IndexIQ (New York Life Investments). Few know the ETF creation-and-redemption process better than Chris.

I want to give you a feel for what is happening on the front lines and asked him if I could share his note with you. Here it is:

Subject: The Fed has WOKE the market....again

The last several sessions, we have seen good strength in the US equity markets HOWEVER, while most of the moves were positive, the recent days where we have had moves up and down as high as 5% in the market were NOT accompanied with heavy volumes. Historically, days that have ranges in excess of 2% (especially days in which the market swings back and forth 2 or 3 times) will have significant volume increases.

From February 24 through March 27 (THE PEAK PANIC) the total value traded in US equity markets was averaging $687 billion per day with ETFs at about 37% of that volume. As a reference, the average from Jan 1 through Feb 20 was only $367 billion per day. The past 5 years the average has been $287 billion per day.

Do you see that? $687 billion AVERAGE versus $287 billion! It persisted for a month!

Back to the last 8 sessions from March 30th through April 8th: The dollar value traded dropped from an average of $687 billion per day to $480 billion per day DESPITE that fact that the markets were incredibly volatile, the news cycle was far from quiet, and economic indicators such as jobless claims were absolutely blasting through estimates. It was strange to think that all of a sudden, things settled back to a sense of normalcy without any real news to support it.

HERE WE ARE TODAY (Thursday April 9): It happened. Whether it is oil futures today selling off 9%, ripping up 13%, dropping 12% and still bouncing up and down like a superball (that’s just today, so far), OR whether it was the Fed announcing that it will purchase high yield bonds and ETFs, the market has WOKE with respect to real volumes. Today’s volumes are actually on par with those experienced during that height of market activity between February 24 and March 27.

Spreads: During the period (Feb 24-Mar 27) we saw high yield and investment grade bonds ETFs drop to discounts north of 5% to the NAV (net asset value of the fund), something that had never before been seen (at least for the extended period of time accompanied with massive flows). Additionally, we saw high-yield muni ETFs drop to 15% and 20% discounts.

For high-yield and investment grade, later in the month of March (post FED purchase program announcement) and into April those discounts actually swung to premiums. Some of those ETFs actually had 5% premiums. Again, this had never been seen before.

Welcome to today: High-yield ETFs have once again blasted through to a 5% premium on massive volumes, as the Fed will be active buyers.

Even high-yield muni funds are trading with little or no premium or discount (haven’t seen that in a while!). Until now there was no guidance from the fed that they would extend their buy program into the high-yield market.

Where from here? You tell me. It feels like society was dropped from the sky into a massive field of land mines. We have been asked to STOP MOVING because every time we move something blows up. So people have frozen in place to prevent accidents from happening. As a result, the number of explosions is lower, BUT we are all still standing in the middle of this field of land mines. HOW DO WE TIP TOE out of this without setting off another cascading string of explosions?

SB here: Why is a HY ETF trading at a 5% premium? Because a buyer who cares little about price or value is buying the ETFs. That buyer is the Fed, armed with a pool of capital from a newly created SPV. I, like you, am trying to figure this out. To me, it feels like a sucker punch to the gut.

"This world runs on individuals pursuing their separate interests. The great achievements of civilization have not come from government bureaucrats. Einstein didn’t discover his theory of relativity on an order from a bureaucrat. Henry Ford didn’t revolutionize the automobile industry that way. In the only cases the masses have escaped the grinding poverty you’re talking about, the only cases in recorded history are where they’ve had capitalism and largely free trade. If you want to know where the masses are worse off, it is exactly the kinds of societies that depart from that. So the record of history is absolutely crystal clear, there is no alternative way, so far discovered, of improving the lives of ordinary people that can hold a candle to the productive activities that are unleashed by a free enterprise system."

– Milton Friedman on the Phil Donahue Show, 1979 (video here)

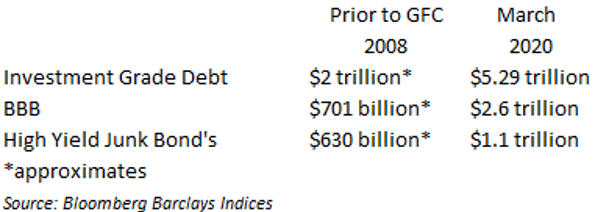

Modern Monetary Theory. Also known as the Magic Money Tree. Trillions in newly invented SPVs. Flood the system with liquidity. Buy up the bonds of good companies, buy up the bad. Those bonds then sit on the books at the Fed, tucked inside those SPVs.

If a junk bond defaults, who’s taking that risk? You are. I am. We taxpayers are taking that risk. And what about that new, freshly printed money? For now, the Fed has hired BlackRock to buy bonds. Yesterday, someone put in a massive order to buy JNK (the SPDR high-yield junk bond ETF). My sources are pretty sure it was the Fed. No wonder it spiked to a 5% premium over its fair value. Who’s the fiduciary now? And what might the managers of JNK do with all that new cash? Inject it into the system. They’ll use it to buy more bonds. They have to by mandate. Where is fair value? Where is price discovery?

I’ve long felt that the exit to the massive global debt mess is a “debt jubilee.” Governments print money, buy up the debts and put them on their balance sheets. Government debts, mortgage debts, student loan debts, corporate debts… not sure where it ends. Didn’t think they’d be buying up junk bonds. And with that, they die. Poof. But the debt of the government’s balance sheet explodes. Whether we like it or not, the game that is being played.

On the other side of this, there will be consequences. The most probable is inflation. For now, we fight deflation and tools that risk future inflation. A delicate balance. I can’t see how they balance deflationary pressures with inflationary medicine. Get it just right, maybe we get through the cave in ok shape. I don’t for the life of me believe they can balance it just right. How big is enough? We are at the beginning of the great debt jubilee. We should set game plan with exit in mind. And we should be well aware of Pandora’s Box we’ve opened and consider the future misbehavior that has been enabled.

My vote is for capitalism, free markets, and individuals in pursuit of their best interests. I don’t mean that in a selfish way. I believe if you advance an idea, build a business, bring like-minded others into your vision, and expand your teams, you create together, grow together, you win and everyone around you wins. Yes, we must also help those in need. We have a human obligation to help those most in need. But we must enable and not suppress.

If one doesn’t have risk of loss, then leverage like crazy and go for your big win. But should I pay for your loss? That is what is happening here. I believe we are better off with millions of us making decisions in a free market than just ceding to a decision made by few for the many. Capitalism is not perfect, but I think Friedman is right. Show me a better system.

Enough of my rant. A special hat tip to my friend Chris. I need another drink.

Let’s look at the economy and the markets. The following is from CNBC:

Ray Dalio predicts a coronavirus depression: ‘This is bigger than what happened in 2008’

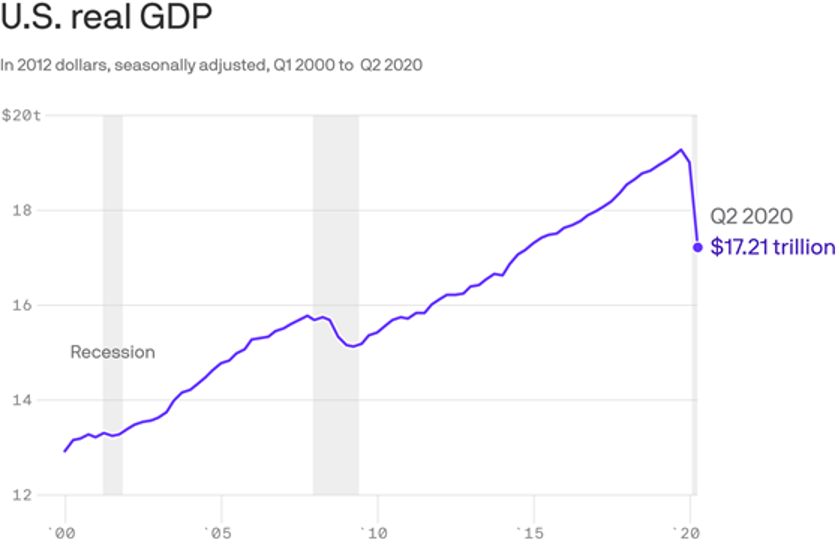

Many economists are predicting that the ongoing economic disruptions and business shutdowns caused by the coronavirus pandemic will result in a global recession. But billionaire investor Ray Dalio is going one step further by predicting a depression.

Dalio — who runs the world’s largest hedge fund, Bridgewater Associates — sees the coming economic downturn as resembling the effects of the Great Depression, which lasted from 1929 to 1933 and is regarded as the worst economic crisis in American history. The Great Depression saw U.S. unemployment hit a peak of nearly 25%, while gross domestic product (GDP) declined by nearly 30%.

“Do I think we’re in that? Yes,” Dalio said when asked about the prospect of a modern depression in a video interview on Wednesday with the “Ted Connects” program, part of the Ted talks platform. The hedge fund billionaire pointed to the likelihood that the U.S. will see a “double-digit unemployment rate” and more than 10% decline in the economy, with effects potentially lasting years rather than months.

A recession sees an economy’s production, reflected in its GDP, decline for multiple quarters in a row, with effects lasting several months. In a depression, though, the effects typically last for a few years.

“I think you could look at this like a tsunami that’s hit — the virus itself and the social distancing — and then what are the consequences in terms of the wreckage [from that],” Dalio said in the interview. He sees the “wreckage” as the long-term effects on businesses’ balance sheets and individuals’ incomes that are taking “tremendous” hits in cases where workers have been laid off.

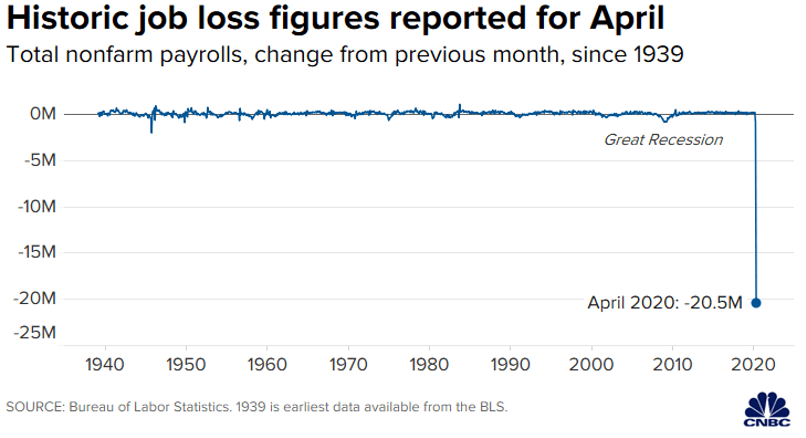

While we still don’t know exactly what the long-term effects of the coronavirus pandemic will be on the global economy, roughly 16 million Americans (about 10% of the overall workforce) have already filed for unemployment benefits in recent weeks. And Goldman Sachs has predicted that U.S. unemployment could hit 15% by this summer, while the financial giant is also bracing for a GDP decline of 34% in the second quarter of 2020.

I think my friend Chris is right. There are minefields all around us. Keep your investment risk-management game plan firmly in place.

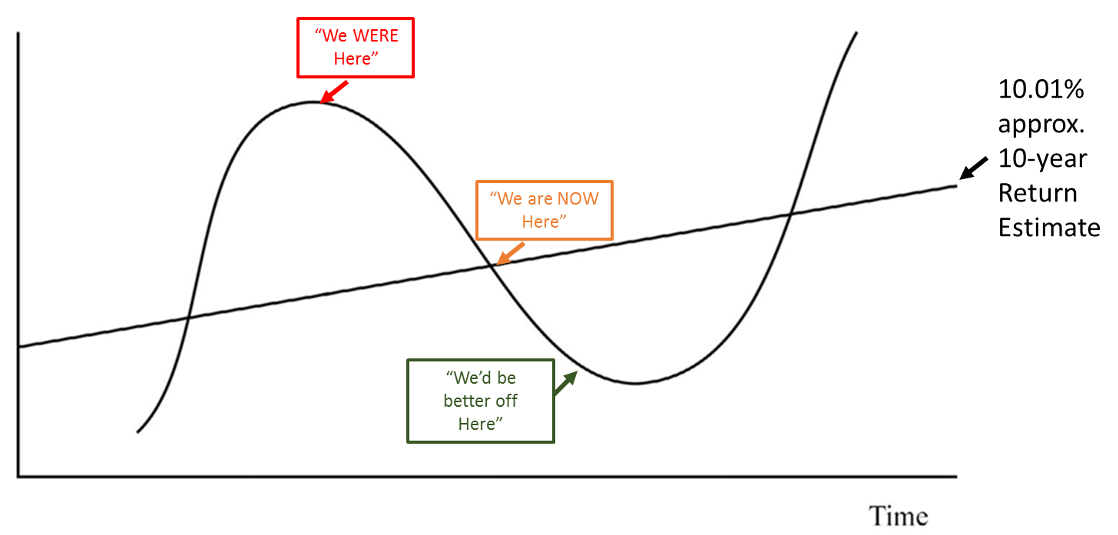

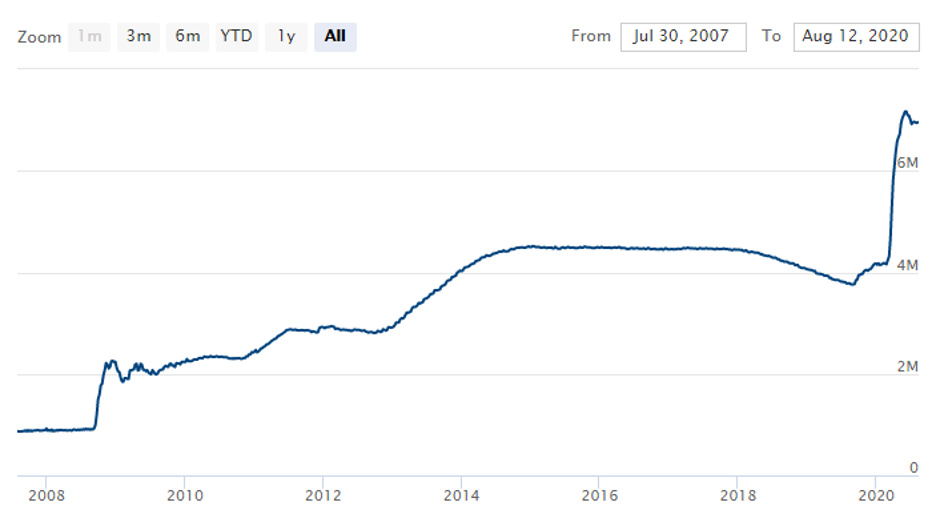

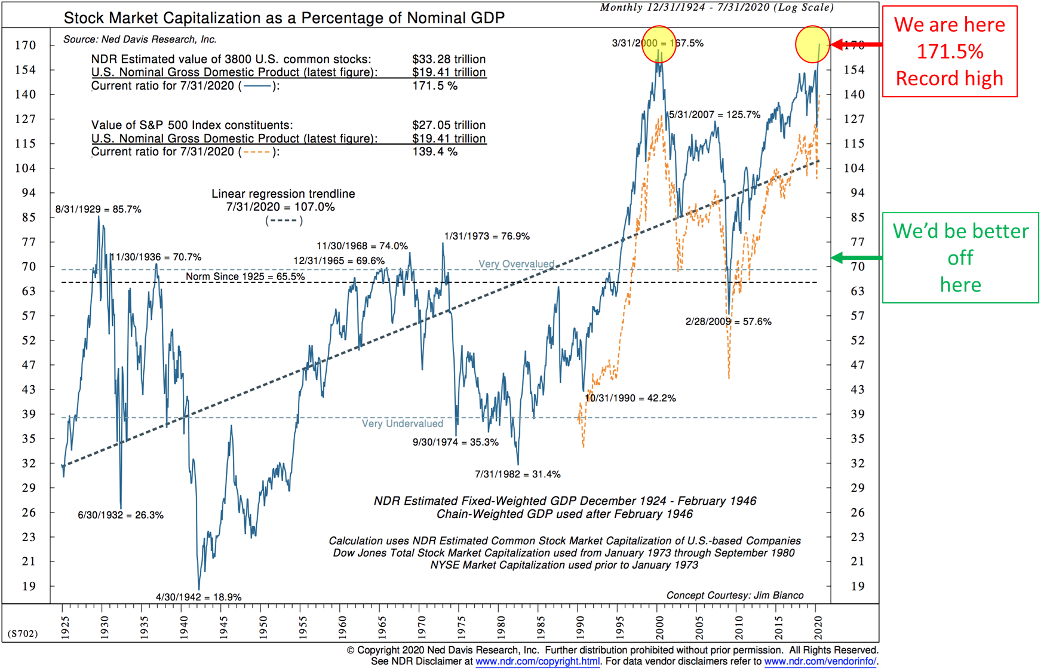

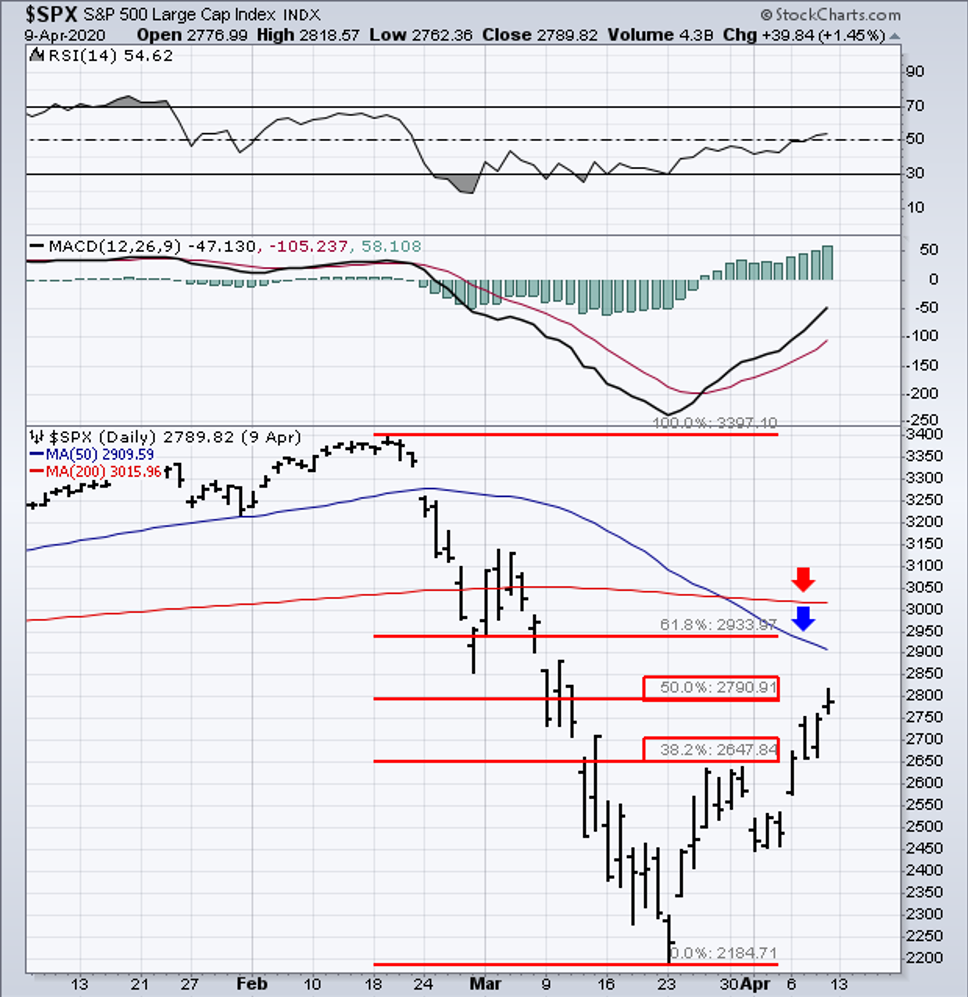

As for the markets, the following chart shows the stock market has recovered 50% of its decline and has reached the upper end of what I’d consider logical resistance at 2,800. The S&P 500 Index declined from approximately 3,400 to 2,200. It hit a high of 2,818 yesterday (April 9, 2020). The next level of resistance is at 2,933. I don’t believe we are out of the woods. I believe we will retest recent lows. I could be wrong. My plan is to add to equities on a retest.

Arts and Entertainment

Arts and Entertainment Business and Industry

Business and Industry Computer and Electronics

Computer and Electronics Games

Games Health

Health Internet and Telecom

Internet and Telecom Shopping

Shopping Sports

Sports Travel

Travel More

More