This site did not show evidence of storing passwords in plaintext.

This site does allow secured connections (https)

This site did show a clear way to unsubscribe from their emails

This site does verify your email address.

Membership Emails

Below is a sample of the emails you can expect to receive when signed up to National Institute of Economic and Social Research.

Pay growth at 11-year high but further acceleration unlikely

Figure 1: Average Weekly Earnings (3 months average year on year growth, per cent)

Source: NIESR, ONS.

Main points

According to new ONS statistics published this morning, UK average weekly earnings (AWE) expanded by 3.6 per cent excluding bonuses

(3.4 per cent including bonuses) in the three months to May compared to the year before (figure 1).

With CPI inflation at 2 per cent in the three months to May, real wages excluding bonuses grew at an annual rate of 1.6 per cent over

the same period, the strongest rate of regular real earnings growth since November 2016 (figure 2).

Our Wage Tracker published last month had suggested that wage growth would continue to pick up modestly in May. This is confirmed by May data outturns which came in slightly stronger

than predicted, partly as a result of upward revisions to April data.

Going forward, the Wage Tracker indicates that regular pay growth will have reached 3.8 per cent in the second quarter of this year. Our first estimate for the third quarter of this

year has regular pay growth stabilising at around 3� per cent, reflecting survey evidence of a reduction in hiring and fewer vacancies.

Based on NIESR Wage Tracker and GDP Tracker information, we estimate unit labour cost growth of around 3 per cent in the second and third quarter of 2019, up from just above 2 per cent

in the first quarter.

Arno Hantzsche, senior economist at NIESR, said

�Strong earnings growth in the first half of 2019 helped real pay recover most of the losses incurred since the financial crisis a decade ago. However, economic and political uncertainty pose a considerable risk to hiring activity and, according to our new

estimates, prevent a further acceleration of earnings growth in the months ahead.�

Figure 2: Real whole economy AWE (3

months average year on year growth, per cent)

Source: ONS, NIESR.

Notes: Real pay growth is nominal pay growth deflated by a 3-month moving average of the consumer price index (CPI).

Figure 3: Public and Private sector AWE (3

months average year on year growth, per cent)

Source: ONS, NIESR.

Please find the full analysis in attachment.

For more information please telephone NIESR on 020 7222 7665.

Kind Regards,

Luca

LUCA PIERI

COMMUNICATIONS AND EVENTS CO-ORDINATOR

NATIONAL INSTITUTE OF ECONOMIC AND SOCIAL RESEARCH

2 Dean Trench Street, Smith Square, London SW1P 3HE +44 (0)020-7654-1931 (direct)

| +44 (0)207222-7665 (general)

The National Institute of Economic and Social Research is a company registered in England and Wales (company number 00341010) and a charity registered

in England and Wales (charity registration number 306083).

This email and any attachments are confidential and intended for the addressee only. If you are not the intended recipient you must take no action based on them, nor must you copy or show them to anyone. Please contact the sender if you believe you have received

this email in error.

We have taken reasonable precautions to ensure this communication does not contain viruses. We cannot accept liability for any damage

your system sustains due to software viruses. You should carry out your own information security and virus checks before opening any attachments or following any links. The contents of this email may be intercepted, monitored and/or recorded by a third party.

We exclude any liability arising from any interception.

______________________________________________________________________

This email has been scanned by the Symantec Email Security.cloud service.

For more information please visit http://www.symanteccloud.com

______________________________________________________________________

National Institute of Economic and Social Research�s GDPTracker

Figure

1 -

UK GDP growth (3 months on previous 3 months, per cent)

Main points

�Latest ONS data published this morning indicates that the UK economy contracted by 0.2 per cent in the second quarter of 2019, partly due to less inventory accumulation

than in the first quarter. This outturn was a little weaker than the 0.1 per cent fall in output that we had forecast last month.

�Recent surveys suggest that output was flat in July, with consumer-led service sector expansion being offset by further contractions in manufacturing and construction.

If these trends continue, GDP will grow by around 0.2 per cent in the third quarter (figure 1). That would mean that output is flat throughout the middle of this year.

�Nevertheless, quarterly data is likely to be volatile throughout the year and, with little positive momentum in the economy, there is a significant risk that output

falls again in the third quarter. In that case the economy would be in a recession that began in April.

Dr Garry Young, Director of Macroeconomic Modelling and Forecasting, said

�Economic growth in the United Kingdom was negative in the second quarter of 2019 and is set to remain weak in the third quarter in the face of a global slowdown and continuing Brexit-related uncertainty. Our latest estimate implies that there is a significant

risk that the economy is already in a recession that began in April, and the clear possibility of a more material downturn should there be a no-deal Brexit.�

Please find the full analysis in the document attached

-------------------------------------------------

For more information please telephone NIESR on 020 7222 7665.

Kind Regards,

Paola

PAOLA BUONADONNA

EAD OF COMMUNICATIONS AND ENGAGEMENT

NATIONAL INSTITUTE OF ECONOMIC AND SOCIAL RESEARCH

2 Dean Trench Street, Smith Square, London SW1P 3HE +44 (0)020-7654-1923 (direct)

| +44 (0) 7710 484152 (mobile)

The National Institute of Economic and Social Research is a company registered in England and Wales (company number 00341010) and a charity registered

in England and Wales (charity registration number 306083).

This email and any attachments are confidential and intended for the addressee only. If you are not the intended recipient you must take no action based on them, nor must you copy or show them to anyone. Please contact the sender if you believe you have received

this email in error.

We have taken reasonable precautions to ensure this communication does not contain viruses. We cannot accept liability for any damage

your system sustains due to software viruses. You should carry out your own information security and virus checks before opening any attachments or following any links. The contents of this email may be intercepted, monitored and/or recorded by a third party.

We exclude any liability arising from any interception.

______________________________________________________________________

This email has been scanned by the Symantec Email Security.cloud service.

For more information please visit http://www.symanteccloud.com

______________________________________________________________________

National Institute of Economic and Social Research�s Wage Tracker

Real earnings growth back to pre-Referendum rates but further pick up unlikely in near term

Main points

According to new ONS statistics published this morning, UK average weekly earnings (AWE) expanded by 3.9 per cent excluding bonuses (3.7 per cent including bonuses) in the three months to June

compared to the year before (figure 1).

With CPI inflation at 2 per cent in the second quarter of this year, real wages excluding bonuses grew at an annual rate of 1.9 per cent over the same period, the strongest rate of regular real

earnings growth since May 2016.

June data outturns are in line with forecasts published in our Wage Tracker last month. Strong quarterly data is explained by April pay rises, with weaker quarter 1 data dropping out of the series;

month-on-month earnings growth rates are considerably weaker, in particular in the public sector.

Going forward, the Wage Tracker indicates that regular pay growth will stabilise at around 3� per cent in the third quarter of this year, reflecting a less tight labour market and survey evidence

of a softening in hiring activity.

Based on NIESR Wage Tracker and weak GDP Tracker information, we estimate unit labour cost growth of nearly 4 per cent in the second of 2019 and above 3 per cent in the third quarter, up from

just above 2 per cent in the first quarter This is likely to put upward pressure on consumer prices in the months ahead.

Dr Arno Hantzsche, Principal Economist in Macroeconomic Modelling and Forecasting, said �While real earnings growth has now

returned to pre-referendum rates, the labour market appears to be reaching a turning point, with unemployment no longer falling, the number of job vacancies no longer increasing and companies and workers deterred from bigger employment decisions by Brexit

and global uncertainties.�

Please find the full analysis in attachment.

For more information please telephone NIESR on 020 7222 7665.

Kind Regards,

Paola

PAOLA BUONADONNA

HEAD OF COMMUNICATIONS AND ENGAGEMENT

NATIONAL INSTITUTE OF ECONOMIC AND SOCIAL RESEARCH

2 Dean Trench Street, Smith Square, London SW1P 3HE +44 (0)020-7654-1923 (direct)

| +44 (0) 7710 484152 (mobile)

The National Institute of Economic and Social Research is a company registered in England and Wales (company number 00341010) and a charity registered

in England and Wales (charity registration number 306083).

This email and any attachments are confidential and intended for the addressee only. If you are not the intended recipient you must take no action based on them, nor must you copy or show them to anyone. Please contact the sender if you believe you have received

this email in error.

We have taken reasonable precautions to ensure this communication does not contain viruses. We cannot accept liability for any damage

your system sustains due to software viruses. You should carry out your own information security and virus checks before opening any attachments or following any links. The contents of this email may be intercepted, monitored and/or recorded by a third party.

We exclude any liability arising from any interception.

______________________________________________________________________

This email has been scanned by the Symantec Email Security.cloud service.

For more information please visit http://www.symanteccloud.com

______________________________________________________________________

National Institute of Economic and Social Research�s

GDPTracker

Figure

1 -

UK GDP growth (3 months on previous 3 months, per cent)

Main points

�The UK economy is on course to grow by 0.3 per cent in the third quarter of 2019, a resumption of growth after a 0.2 per cent fall in the second quarter

when production had slackened after being boosted in the first quarter by stockbuilding ahead of the original Brexit departure date (figure 1).

�According to new ONS statistics published this morning, the UK economy was flat in the three months to July. The stagnation in output in the three

months to July was associated with an above-expectations 0.3 per cent increase in GDP in the month of July, driven primarily by an increase in output in the services sector.

�Recent surveys suggest that output was flat in August, with service sector expansion being offset by contractions in manufacturing and construction.

If these trends continue, GDP will grow by around 0.3 per cent in the third quarter (figure 1). This is higher than the 0.2 per cent growth that we had pencilled in last month.

Dr Garry Young, Director of Macroeconomic Modelling and Forecasting, said:

�It looks like there has been a welcome resumption of economic growth in the third quarter, roughly offsetting the fall in the second quarter. But it is not clear how long growth will

continue. Only the services sector is expanding, primarily to meet higher demand from consumers driven by increased household incomes fuelled by rising real wages. But there is a limit to how much further real wages can grow without a pick-up in investment

and productivity, and this seems unlikely in the near term.�

Please find the full analysis in the document attached

-------------------------------------------------

For more information please telephone NIESR on 020 7222 7665.

Kind Regards,

Paola

PAOLA BUONADONNA

EAD OF COMMUNICATIONS AND ENGAGEMENT

NATIONAL INSTITUTE OF ECONOMIC AND SOCIAL RESEARCH

2 Dean Trench Street, Smith Square, London SW1P 3HE +44 (0)020-7654-1923 (direct)

| +44 (0) 7710 484152 (mobile)

The National Institute of Economic and Social Research is a company registered in England and Wales (company number 00341010) and a charity registered

in England and Wales (charity registration number 306083).

This email and any attachments are confidential and intended for the addressee only. If you are not the intended recipient you must take no action based on them, nor must you copy or show them to anyone. Please contact the sender if you believe you have received

this email in error.

We have taken reasonable precautions to ensure this communication does not contain viruses. We cannot accept liability for any damage

your system sustains due to software viruses. You should carry out your own information security and virus checks before opening any attachments or following any links. The contents of this email may be intercepted, monitored and/or recorded by a third party.

We exclude any liability arising from any interception.

______________________________________________________________________

This email has been scanned by the Symantec Email Security.cloud service.

For more information please visit http://www.symanteccloud.com

______________________________________________________________________

National Institute of Economic and Social Research�s Wage Tracker

Strong earnings data driven by July bonuses and public sector pay but further pick-up unlikely

Figure 1 � Average weekly earnings growth (per cent per annum)

Main points

� According to new ONS statistics published this morning, UK average weekly earnings (AWE) expanded by 3.8 per cent excluding bonuses (4 per cent including bonuses) in the three months

to July compared to the year before (figure 1).

� With CPI inflation at 2 per cent in the three months to July, real wages excluding bonuses grew at an annual rate of 1.8 per cent over the same period (2 per cent including bonuses).

� July total earnings data was slightly stronger than we forecast last month due to above-expectation bonus payments, more robust public sector earnings, and back data revisions while

data on private sector regular earnings turned out as forecast.

� Going forward, the Wage Tracker indicates that regular pay growth will stabilise at just below 4 per cent in the third quarter of this year, reflecting survey evidence of a softening

in hiring activity.

� Based on NIESR Wage Tracker and GDP Tracker information, we estimate unit labour cost growth of around 3� per cent in the third quarter as economic activity remains lacklustre. There

is a risk that firms pass higher production costs on to consumers which could add to inflationary pressures in the economy.

Dr Arno Hantzsche, Principal Economist in Macroeconomic Modelling and Forecasting, said �Today�s labour market data were again strong but more timely signals show that a turning point may

soon be reached as Brexit and global uncertainties increasingly weigh on hiring. Whole-economy earnings growth has become more reliant on services sectors whose output continues to be in strong demand and on hiring and pay decisions in the public sector.�

Please find the full analysis in attachment.

For more information please telephone NIESR on 020 7222 7665.

Kind Regards,

Paola

PAOLA BUONADONNA

HEAD OF COMMUNICATIONS AND ENGAGEMENT

NATIONAL INSTITUTE OF ECONOMIC AND SOCIAL RESEARCH

2 Dean Trench Street, Smith Square, London SW1P 3HE +44 (0)020-7654-1923 (direct)

| +44 (0) 7710 484152 (mobile)

The National Institute of Economic and Social Research is a company registered in England and Wales (company number 00341010) and a charity registered

in England and Wales (charity registration number 306083).

This email and any attachments are confidential and intended for the addressee only. If you are not the intended recipient you must take no action based on them, nor must you copy or show them to anyone. Please contact the sender if you believe you have received

this email in error.

We have taken reasonable precautions to ensure this communication does not contain viruses. We cannot accept liability for any damage

your system sustains due to software viruses. You should carry out your own information security and virus checks before opening any attachments or following any links. The contents of this email may be intercepted, monitored and/or recorded by a third party.

We exclude any liability arising from any interception.

______________________________________________________________________

This email has been scanned by the Symantec Email Security.cloud service.

For more information please visit http://www.symanteccloud.com

______________________________________________________________________

NIESR October 2019 Newsletter

View this email in your browser

National Institute of Economic and Social Research

Newsletter - October 2019

Welcome to NIESR�s newsletter, a quarterly catch-up with the main publications, events and media stories the Institute has been involved with and a look ahead to what we are planning for the next quarter.

The Festival of Social Sciences at NIESR

The ESRC Festival of Social Science 2019 will run from 2-9 November 2019, with over 470 events being held across the UK, providing an opportunity for the public to meet some of the country�s leading social scientists to discover, discuss and debate how research affects their lives.

This year, NIESR is delighted to be taking part by putting on its largest series of events yet: �The Festival of Social Science at NIESR', running from 4 to 9 November. Here are some highlights:

4 November - Inaugural Prais Lecture on Productivity: How not to miss the productivity revival once again with Bart Van Ark (Chief Economist at The Conference Board, New York).

6 November - Inaugural Dow Lecture: Do economists expect too much from expectations? with Martin Weale.

7 November - Is it a bad idea to be a football fan? with Peter Dolton.

Our full list of events and RSVP details can be found here.

Economic Review No.249 - "Economic Measurement"

Our quarterly Review, published on the 24th of July, focused on economic measurement and emerged from research presented at the ESCoE 2019 Conference on Economic Measurement.Andrew Aitken's article on "Measuring welfare beyond GDP" is free for all to read and blogs have appeared on our website since with the highlights of all the articles behind the paywall. "Dutch imports: used in the economy or re-exported?" by Oscar Lemmers, has proved particularly popular.

By special arrangement with our publishers our latest assessments of the UK and World economy can be read free of charge in their entirety here. Our UK forecast, with its recession warning, received an extraordinary level of media coverage. This comment piece by our Director Jagjit Chadha (originally produced for the New Statesman) sums up the economic situation inherited by the new Prime Minister.

Other research highlights and papers

Thanks to the IAA funding from the ESRC we have started to produce Topical Briefings reviewing the evidence or updating our analysis on a variety of economic and social issues. Our first three Briefings are:

Overview of evidence on UK public attitudes to immigration, by Johnny Runge Overview of evidence on economic impacts of EU immigration, by Johnny Runge Industry and Regional Effects of a No-Deal Brexit, by Arno Hantzsche

We released a number of other reports, including two new reports with Impetus contributing to the Youth Jobs Gap research series, which uses new Longitudinal Education Outcomes data to present new insights into disadvantaged young people�s transition from compulsory education into employment.

The Employment Gap in the West Midlands, by Stefan Speckesser and Hector Espinoza

The Employment Gap in the North West, by Stefan Speckesser and Hector Espinoza

Recent Discussion Papers include:

The Indeterminacy Agenda in Macroeconomics, by Roger Farmer

Tax Policy for Innovation, by Bronwyn Hall

Some International Evidence for Keynesian Economics Without the Phillips Curve, by Roger Farmer and Giovanni Nicolo'

We continued to produce monthly GDP Trackers (you can see past releases and the schedule for future releases here) and monthly Wage Trackers (find past releases and the schedule for future releases here). You can also subscribe to receive updates on new Discussion Papers; find all of our subscription options here.

Blog highlights

Aside from comments relating to the Review, we also published a number of popular blogs by our researchers including:

"What would lead us to revise our Brexit impact estimates? It�s the politics, stupid �" by Arno Hantzsche;

"New immigration policy: a bitter pill to swallow for those who give us our daily bread", by Heather Rolfe;

"Why the Chancellor will not meet the fiscal mandate", by Arno Hantzsche and Garry Young;

"Freeports, like free lunches, might come with strings attached", by Marta Paczos;

"A Governor for our Brexit Times", by Jagjt Chadha;

"Policy in the age of Global Value Chains: what is the way forward?", by Marta Paczos and Ana Rincon-Aznar.

Events this past quarter

We has a really busy summer. Highlights of our events include an all-day workshop on "Global Value Chains: Current developments and implications for Europe" in early June with Innovate UK and Coriolis, which brought together the work by leading European research institutes, international organizations and private sector initiatives to discuss and identify the most relevant research and policy priorities for the near future. The three sessions were live-streamed and can be watched here, here and here.

A few days alter our library was packed again for David Blanchflower in conversation with Dr Gertjan Vlieghethe about his latest book: "Not Working - Where Have All the Good Jobs Gone?" A live-stream of what proved a very lively event is available here.

Later that month the second Anglo-German Foundation Lecture supported by NIESR took place at the DIW Institute in Berlin. Profesor David Miles presented "How unfair is GDP? The half-life of Economic Injustice".

In July we held several events linked to our latest Review, including a press conference, and Briefings for Economists and Embassies. Members of our Macro Team travelled to St Louis for a workshop on "Modelling the macroeconomy in risky times" organised jointly by NIESR, the OMFIF Foundation, the Centre for Macroeconomics, the Federal Reserve Bank of St Louis, and the Olin School of Business.

Last but not least on 14th August we held our second Business Conditions Forum, comprising of chief economists and senior economists from major survey organisations, economists from the official sector, and NIESR economists with a special interest in the UK. After exploring the impact of uncertainty on the UK economy in its meeting in May, this time the Forum asked whether the labour market is turning. You can find a summary of the discussion here.

Forthcoming events

Aside from the special events of the Festival of Social Sciences Week, featured above, we will be hosting a number of targeted briefings and workshops as well as public seminars.

14 October - Beyond Brexit: a programme for EU reform - This seminar will give a preview of policy ideas from the November 2019 NIESR Economic Review and will feature a panel of contributing authors including Jeremy Greenstock, Kate Barker and Tim Besley. Please find further details and RSVP contact here.

15 October - The 2019 Monetary and Financial Policy Conference held at Bloomberg HQ and co-hosted by NIESR will feature a session dedicated to the monetary policy framework here in the UK. In that session our Director, Jagjit Chadha, will present an e-book proposing a series of reforms that the Chancellor and the next Governor of the Bank should consider. You can register for the conference here.

29 October - We'll welcome journalists at our quarterly press conference to unveil our next UK and World forecasts (to be published the following day in NIESR's November Economic Review).

30 October - Economists' Briefing about our latest forecasts.

More information about what is coming up is available on our Events page.

Supporting NIESR

Now in its 82nd year, the Institute continues to be the truly independent voice of economics, carrying out research into the economic and social forces that affect people�s lives while receiving no core funding from government or other sources. You can support the Institute in its mission to shape and challenge policy in these uncertain times by becoming a Corporate Member.

Read herefor more information about the advantages of joining our Corporate Members' scheme and do not hesitate to contact our Director, Professor Jagjit Chadha, or get in touch to discuss what NIESR can do for you.

Copyright � 2018 NIESR, All rights reserved.

You can update your preferences or unsubscribe from this list

National Institute of Economic and Social Research�s

GDPTracker

Figure

1 -

UK GDP growth (3 months on previous 3 months, per cent)

Main points

�The UK economy is on course to grow by 0.5 per cent in the third quarter of 2019 and by 0.3 per cent in the fourth quarter (figure 1). This would be

consistent with GDP growth of 1.3 per cent in 2019 as a whole, down slightly from 1.4 per cent in 2018 and 1.9 per cent in 2017.

�According to new ONS statistics published this morning, the UK economy grew by 0.3 per cent in the three months to August, driven by growth in the services

sector. This was a little stronger than we forecast last month, partly reflecting upward revisions to the June and July data. GDP fell by 0.1 per cent in the month of August, in line with our previous forecast.

�Recent surveys suggest that private sector output fell in September, with manufacturing being particularly weak. Nevertheless, even after pencilling

in flat output in September, we forecast GDP growth of 0.5 per cent in the quarter as a whole as the economy recovers from the particularly weak second quarter.

Dr Garry Young, Director of Macroeconomic Modelling and Forecasting, said : �Despite

better than expected GDP data, the underlying pace of growth in the United Kingdom is slow. The strongest source of private sector demand is household consumption, driven by real wage growth, but this is not sustainable without a pick-up in productivity growth,

and this seems unlikely in the near term.�

Please find the full analysis in the document attached

-------------------------------------------------

For more information please contact Luca Pieri on l.pieri@niesr.ac.uk or on 07405496121.

Kind Regards,

The Comms Team

PAOLA BUONADONNA

EAD OF COMMUNICATIONS AND ENGAGEMENT

NATIONAL INSTITUTE OF ECONOMIC AND SOCIAL RESEARCH

2 Dean Trench Street, Smith Square, London SW1P 3HE +44 (0)020-7654-1923 (direct)

| +44 (0) 7710 484152 (mobile)

The National Institute of Economic and Social Research is a company registered in England and Wales (company number 00341010) and a charity registered

in England and Wales (charity registration number 306083).

This email and any attachments are confidential and intended for the addressee only. If you are not the intended recipient you must take no action based on them, nor must you copy or show them to anyone. Please contact the sender if you believe you have received

this email in error.

We have taken reasonable precautions to ensure this communication does not contain viruses. We cannot accept liability for any damage

your system sustains due to software viruses. You should carry out your own information security and virus checks before opening any attachments or following any links. The contents of this email may be intercepted, monitored and/or recorded by a third party.

We exclude any liability arising from any interception.

______________________________________________________________________

This email has been scanned by the Symantec Email Security.cloud service.

For more information please visit http://www.symanteccloud.com

______________________________________________________________________

National Institute of Economic and Social Research�s Wage Tracker

Labour market weathering an increasingly difficult economic environment

Figure 1 � Average weekly earnings growth (per cent per annum)

1 �

Average weekly earnings growth (per cent per annum

Main points

According to new ONS statistics published this morning, UK average weekly earnings (AWE) expanded by 3.8 per cent (excluding and including bonuses) in the three months to August

compared to the year before (figure 1).

With CPI inflation at 1.9 per cent in the three months to August, real wages grew at an annual rate of 1.9 per cent over the same period.

Private sector earnings data in August turned out to be in line with the estimate published in our Wage Tracker last month and public sector earnings data was only slightly weaker.

The Wage Tracker indicates that regular earnings growth will have stabilised at an annual rate of 3.8 per cent in the third quarter and is expected to remain largely unchanged

in the fourth quarter.

Based on NIESR Wage Tracker and GDP Tracker information, we estimate unit labour cost growth of around 3� per cent per annum in the third and fourth quarters

of 2019 while economic activity remains lacklustre.

Dr Arno Hantzsche, Principal Economist in Macroeconomic Modelling and Forecasting, said ��In the economy as a whole, employment and wage growth are now stabilising amidst global and domestic

uncertainties. While sectors engaging in international trade increasingly face difficulties, also affecting hiring and pay, domestically active service sectors are so far withstanding the economic challenges.�

NATIONAL INSTITUTE OF ECONOMIC AND SOCIAL RESEARCH

2 Dean Trench Street, Smith Square, London SW1P 3HE +44 (0)020-7654-1923 (direct)

| +44 (0) 7710 484152 (mobile)

The National Institute of Economic and Social Research is a company registered in England and Wales (company number 00341010) and a charity registered

in England and Wales (charity registration number 306083).

This email and any attachments are confidential and intended for the addressee only. If you are not the intended recipient you must take no action based on them, nor must you copy or show them to anyone. Please contact the sender if you believe you have received

this email in error.

We have taken reasonable precautions to ensure this communication does not contain viruses. We cannot accept liability for any damage

your system sustains due to software viruses. You should carry out your own information security and virus checks before opening any attachments or following any links. The contents of this email may be intercepted, monitored and/or recorded by a third party.

We exclude any liability arising from any interception.

______________________________________________________________________

This email has been scanned by the Symantec Email Security.cloud service.

For more information please visit http://www.symanteccloud.com

______________________________________________________________________

View this email in your browser

View the latest discussion papers from the

National Institute of Economic and Social Research

"Below the Aggregate: A Sectoral Account of the UK Productivity Puzzle" by Rebecca Riley, Ana Rincon-Aznar and Lea Samek. Read more here...

"A Century of High Frequency UK Macroeconomic Statistics: A Data Inventory" by Jagjit S Chadha, Ana Rincon-Aznar, Sally Srinivasan and Ryland Thomas. Read more here...

"The evolution of tax implicit value judgements, redistribution and income inequality in the UK: 1968 to 2015" by Justin Van de Ven and Nicolas H�rault. Read more here...

"What does leadership look like in schools and does it matter for school performance?" by Alex Bryson, Lucy Stokes and David Wilkinson. Read more here...

"Below the Aggregate: A Sectoral Account of the UK Productivity Puzzle" by Rebecca Riley, Ana Rincon-Aznar and Lea Samek Discussion Paper no.508

We analyse new industry-level data to re-examine the UK productivity puzzle. We carry out an accounting exercise that allows us to distinguish general macroeconomic patterns from sector trends and idiosyncrasies, providing a roadmap for anyone interested in explaining the puzzle. We focus on the UK market sector. Average annual labour productivity growth was 2.5 percentage points lower during the period 2011-2015 than in the decade before the financial crisis that began in 2007. We find that several years on from the financial crisis stagnation remains widespread across detailed industry divisions, pointing to economy-wide explanations for the puzzle. With some exceptions, labour productivity growth lost most momentum in those industries that experienced strong growth before the crisis. Three fifths of the gap is accounted for by a few industries that together account for less than one fifth of market sector value added. In terms of why we observe continued stagnation, we find that capital shallowing has become increasingly important in explaining the labour productivity growth gap in service sectors, as the buoyancy of the UK labour market has not been sufficiently matched by investment, although our figures suggest that the majority of the productivity gap is accounted for by a TFP gap. The collapse in labour productivity growth has been more pronounced in the UK than elsewhere, but the broad sector patterns of productivity stagnation are in many respects similar across other advanced economies, emphasising the importance of global explanations for the puzzle. UK industries that saw the biggest reductions in productivity growth tended to be internationally competitive and more dependent on global demand than other industries. They were also industries where productivity is difficult to measure.

Read the full paper

"A Century of High Frequency UK Macroeconomic Statistics: A Data Inventory" by Jagjit S Chadha, Ana Rincon-Aznar, Sally Srinivasan and Ryland Thomas Discussion Paper no.509

This paper provides an inventory of the available macroeconomic statistics in the UK for the last hundred years or so. The focus is on documenting the higher frequency (daily, monthly and quarterly) macroeconomic data that are available after the World War 1, rather than longer run annual time series which has been the focus of other collections. It discusses some of the challenges that need to be overcome in order to create a continuous historical dataset over this period. The inventory follows the structure of the Economic Trends Annual Supplement (ETAS) that was produced for many years by the Office for National Statistics. It covers statistics on National Accounts, prices, labour market indicators, selected demand and output indicators and financial market data (including money and credit aggregates). Using this structure the paper explores to what extent it is possible to create a consistent, usable and comprehensive high frequency macroeconomic dataset back to the 1920s and earlier.

Read the full paper

"The evolution of tax implicit value judgements, redistribution and income inequality in the UK: 1968 to 2015" by Justin Van de Ven and Nicolas H�rault Discussion Paper no.510

An issue of interest in the literature that explores the drivers of inequality is the distributional bearing of tax and transfer policy, where an important theme concerns changes in the relative treatment of alternative population subgroups. We develop an empirical approach for quantifying the value judgements implicit in the relative treatment of demographic subgroups by a tax and transfer system. We apply this approach to UK data reported at annual intervals between 1968 and 2015, documenting remarkable improvements in tax and transfer treatment enjoyed by some population subgroups � particularly families with children and age pensioners � relative to the wider population. We show that accounting for the changing value judgements implicit in tax and transfer policy provides a fresh perspective on the evolution of income inequality and redistribution; one that departs from the prevailing view that UK inequality stopped rising from the early 1990s.

Read the full paper

"What does leadership look like in schools and does it matter for school performance?" by Alex Bryson, Lucy Stokes and David Wilkinson Discussion Paper no.511

We consider the role played by school leaders in improving pupil attainment, going beyond previous studies by exploring the leadership roles of deputy and assistant heads and classroom-based teachers with additional leadership responsibilities. Using panel data for state-funded secondary schools in England for the period 2010/11-2015/16 we find academy schools typically employ more staff in leadership roles than community schools. Increases in the number of staff in leadership roles below headship level are associated, at least to some extent, with improved school performance in Single Academy Trusts, but this is not the case for schools that are part of Multi Academy Trusts. Our findings suggest that the potential benefits of distributing leadership within schools may only be realised when leaders have sufficient autonomy.

Read the full paper

Don't forget to sign up to receive all our latest updates

Become a Corporate Sponsor

National Institute of Economic and Social Research

2 Dean Trench Street

Smith Square

London

SW1P 3HE

P: +44 (0) 207 222 7665

Copyright � 2019 NIESR, All rights reserved.

You can update your preferences or unsubscribe from this list

National Institute of Economic and Social Research�s

GDPTracker

Figure

1 -

UK GDP growth (3 months on previous 3 months, per cent)

Main points

�The UK economy grew by 0.3 per cent in the third quarter of 2019 and is on course to grow by 0.2 per cent in the fourth quarter (figure 1). This would be consistent with GDP growth

of 1.2 per cent in 2019, down slightly from 1.4 per cent in 2018.

�According to new ONS statistics published this morning, the UK economy grew by 0.3 per cent in the third quarter, driven by growth in the services sector. This was a little weaker

than we had forecast last month, partly reflecting downward revisions to the July and August data. GDP fell 0.1 per cent in the month of September, the second consecutive monthly fall, slightly weaker than our previous forecast.

�Recent surveys suggest that private sector output was flat in October. Nevertheless, we are expecting some growth in public sector output and so are forecasting growth of 0.2 per

cent in the fourth quarter.

Dr Garry Young, Director of Macroeconomic Modelling and Forecasting, said:

�The latest data confirm that the underlying pace of growth in the United Kingdom is slow, reflecting weak business investment growth. GDP fell slightly in August and September and the latest surveys point to further stagnation at the

end of the year. The economy is being held back by weak productivity growth and low investment due to chronic levels of uncertainty.�

Please find the full analysis in the document attached

-------------------------------------------------

For more information please contact Luca Pieri on

l.pieri@niesr.ac.uk or on 0207 654 1931.

Kind Regards,

The Comms Team

----------------------------------

LUCA PIERI

RESEARCH COMMUNICATION MANAGER

NATIONAL INSTITUTE OF ECONOMIC AND SOCIAL RESEARCH

2 Dean Trench Street, Smith Square, London SW1P 3HE +44 (0)020-7654-1931 (direct)

| +44 (0)207222-7665 (general)

The National Institute of Economic and Social Research is a company registered in England and Wales (company number 00341010) and a charity registered

in England and Wales (charity registration number 306083).

This email and any attachments are confidential and intended for the addressee only. If you are not the intended recipient you must take no action based on them, nor must you copy or show them to anyone. Please contact the sender if you believe you have received

this email in error.

We have taken reasonable precautions to ensure this communication does not contain viruses. We cannot accept liability for any damage

your system sustains due to software viruses. You should carry out your own information security and virus checks before opening any attachments or following any links. The contents of this email may be intercepted, monitored and/or recorded by a third party.

We exclude any liability arising from any interception.

______________________________________________________________________

This email has been scanned by the Symantec Email Security.cloud service.

For more information please visit http://www.symanteccloud.com

______________________________________________________________________

National Institute of Economic and Social Research�s Wage Tracker

Figure 1 � Average weekly earnings growth (per cent per annum)

1 �

Average weekly earnings growth (per cent per annum

Main points

According to new ONS statistics published this morning, UK average weekly earnings (AWE) expanded by 3.6 per cent (excluding and including bonuses) in the three months to September compared to the year before

(figure 1).

With CPI inflation at 1.8 per cent in the three months to September, real wages grew at an annual rate of 1.8 per cent over the same period.

Earnings growth was slower in September than at its recent peak in the three months to June and softer than the estimate we published in our Wage Tracker last month. In particular private sector earnings

data was weaker than forecast, partly as a result of downward revisions to past data.

The Wage Tracker indicates that regular earnings growth will remain just above 3� per cent in the fourth quarter of 2019.

Based on NIESR Wage Tracker and GDP Tracker information, we estimate unit labour cost growth of around 3-3� per cent per annum in the fourth quarter, which is somewhat softer than in previous

quarters.

Dr Arno Hantzsche, Principal Economist in Macroeconomic Modelling and Forecasting, said�As the country approaches the general election, hiring activity is continuing to soften and the pace of earnings growth is slowing, suggesting that elevated uncertainty and a lack of growth

momentum are increasingly taking a toll on the labour market�.

______________________________________________________________________

This email has been scanned by the Symantec Email Security.cloud service.

For more information please visit http://www.symanteccloud.com

______________________________________________________________________

National Institute of Economic and

Social Research

General Election 2019 Newsletter

NIESR is aiming to improve the level of public understanding and the quality of media coverage of the key issues facing voters on 12 December.

As well as providing data and illustrative charts, we have published compact briefings that further the understanding of public policy questions while our expert economists have made a number of podcasts and vodcasts. Where manifestos touch on the topics we will integrate a balanced assessment of party policies. You can see a selection of our work below.

Once the dust has settled after the election result, these issues will also be some of the most pressing facing the new government in the months and years to come. So please continue to read these briefings even after the Election. We would like to thank The Nuffield Foundation for their support.

Our Research Briefings focus on:

The Economy and Brexit???

The Current Economic Backdrop

The Fiscal and Macroeconomic Impact of Political Parties� Proposed Policies (two briefings)

The Economic and Fiscal Impact of Brexit

Assessment of Monetary and Fiscal Policy Frameworks

Regions, Productivity and Trade

Places and Spaces: Mapping Britain's Regional Divides

Trade and Trade Policy after Brexit

Education

Education Policy Priorities and a look into the Manifestos

Minimum Wages

Immigration

You can listen to new, snappy 10-minute podcasts of chats between our economists examining four key issues:

Minimum Wages

The Economy

Education Policy

Regional Divides

There is a series of 6 vodcasts where NIESR staff explain some of the key issues in less than three minutes each:

Should we raise the minimum wage?

Are Britain�s skills stagnating?

Does the government need new spending rules?

Has Brexit hurt the economy?

Has Brexit already reduced immigration?

What to do about left-behind places?

NIESR General Election 2019 Website

Subscribe to our newsletters & trackers

Copyright � 2019 National Institute of Economic and Social Research, All rights reserved.

Want to change how you receive these emails?

You can update your preferences or unsubscribe from this list.

National Institute of Economic and Social Research�s

GDPTracker

Figure 1 -

UK GDP growth (3 months on previous 3 months, per cent)

Main points

�The UK economy is on course to grow by 0.1 per cent in the fourth quarter (figure 1). This would be consistent with GDP growth of 1.3 per cent in 2019, down slightly from 1.4 per cent in 2018.

�According to new ONS statistics published this morning, the UK economy grew by 0.0 per cent in the three months to October, this was marginally weaker than the 0.1 per cent growth that we had expected

last month. Output rose slightly in October in the production and service sectors, but dropped unexpectedly sharply in construction.

�Recent surveys suggest that service sector output was little changed in November, with contractions in manufacturing and construction.

Dr Garry Young, Director of Macroeconomic Modelling and Forecasting, said:�The latest data confirm that economic growth in the United Kingdom is petering out at the end of the year. GDP was flat in the three months to October, and the latest surveys point to further stagnation in November and December. The

economy is being held back by weak productivity growth and low investment due to chronic levels of uncertainty.

While some uncertainty could be resolved by the outcome of the general election, it is doubtful that this will provide businesses with the clarity needed to invest with confidence.�

Please find the full analysis in the document attached

-------------------------------------------------

For more information please contact Phil Thornton on

p.thornton@niesr.ac.uk / 0207 654 1923 or Luca Pieri on

l.pieri@niesr.ac.uk/ 079 305 44631

Kind Regards,

The Comms Team

----------------------------------

Check out our General Election 2019 Analysis

The National Institute of Economic and Social Research is a company registered in England and Wales (company number 00341010) and a charity registered

in England and Wales (charity registration number 306083).

This email and any attachments are confidential and intended for the addressee only. If you are not the intended recipient you must take no action based on them, nor must you copy or show them to anyone. Please contact the sender if you believe you have received

this email in error.

We have taken reasonable precautions to ensure this communication does not contain viruses. We cannot accept liability for any damage

your system sustains due to software viruses. You should carry out your own information security and virus checks before opening any attachments or following any links. The contents of this email may be intercepted, monitored and/or recorded by a third party.

We exclude any liability arising from any interception.

______________________________________________________________________

This email has been scanned by the Symantec Email Security.cloud service.

For more information please visit http://www.symanteccloud.com

______________________________________________________________________

View this email in your browser

Season's Greetings from all of us at the

National Institute of Economic and Social Research We'd like to share some of the highlights of 2019 with you, and wish you all the very best for 2020

The General Election

With funding from the Nuffield Foundation, we were once again able produce valuable, balanced research in the lead up to the General Election on the 12th December. With 9 election briefings, 6 vodcasts and 5 podcasts, we were able to look at the issues facing the next government from migration, the economy and regional inequalities (and much more besides).

National Institute Economic Review

Our February Review looked at Productivity and was introduced by our Director, Jagjit S Chadha - "Productivity: Past, Present and Future"

In May, we turned our attention to immigration policy, looking at the "Challenges for Immigration Policy in Post-Brexit Britain" (introduction).

August's edition looked at economic measurement, from measuring welfare to emergent economic activities.

November saw our 250th edition of the Economic Review, looking at the landscape in the UK "Beyond Brexit: A Programme for UK Reform". Featuring a bumper crop of 13 articles, covering trade, foreign policy, infrastructure and much more, the whole journal is free to view to mark our 250 milestone.

From 2020, the Review will be moving publisher from Sage to Cambridge Univerity Press. It would be extremely useful if you could take some time to complete this short surveyon the Review to help shape its future.

Brexit

We continued to cover the Brexit debate, producing a number of important articles and blogs. You can view these on our dedicated Brexit pages here. These included our 250th edition of our Economic Review, with no less than 13 essays on "Beyond Brexit". See the Review section above.

ESRC Impact Acceleration Award

In recognition for its growing profile and its commitment to impact and engagement, NIESR was awarded an Impact Acceleration Account (IAA) from the Economic and Social Research Council in Spring of this year. As part of this, NIESR was delighted to host its first ever Festival of Social Sciences from 4th-9th November. With events ranging from the inaugural lectures of two brand new series to an open lecture on the emotional economics of football fans, it was an engaging and dynamic week. You can view highlights of the week here and take a look at the full programme here.

Research

Some key outputs this year included:

Education & Labour

�Changing Mindsets: Effectiveness trial� - The Changing Mindsets project aimed to improve attainment outcomes at the end of primary school by teaching Year 6 pupils that their brain potential was not a fixed entity but could grow and change through effort exerted.

�Establishing the Employment Gap� - This report establishes for the first time an employment gap between young people from disadvantaged backgrounds and their better-off peers: disadvantaged young people are twice as likely to not be in employment, education or training (NEET).

Employment & Social Policy

�Understanding employers� use of the National Minimum Wage youth rates� � a detailed review of the policies around training, education and support to work for young people, as well as research findings on how employers set pay for young workers (commissioned by the Low Pay Commission)

�Promoting Ethnic and Religious Integration In Schools: A Review of Evidence� - Religious and ethnic segregation in schools is an issue of concern for educationalists and policy makers because it has implications for equality and for inclusion and social cohesion. This report was commissioned by the Department for Education to provide evidence on how segregation might be addressed by reviewing available evidence on approaches in place to promote religious and ethnic integration in education settings.

Macroeconomics

The Macroeconomic and Modelling Team introduced two new �Tracker� services this year, alongside their GDP Tracker. The Wage and CPITrackers are released on the same day as ONS releases. Our UK and World quarterly forecasts are available on our website, as well as our new Business Conditions Forumwhich launched in May 2019.

Trade, Investment & Productivity

�Below the Aggregate: A Sectoral Account of the UK Productivity Puzzle� � In this Discussion Paper, the authors analyse new industry-level data to re-examine the UK productivity puzzle.

�Regional Economic Disparities and Development in the UK� � This policy paper explores the evolution of regional economic disparities in the UK from the 1960s until now.

ESCoE Our partners ESCoE had a busy year, including hosting their second conference on Economic Measurement. More details on ESCoE�s work here. Rebuilding Macroeconomics Rebuilding Macroeconomics also held their second annual conference, to discuss what interdisciplinary research can offer macroeconomics. More details on Rebuilding Macroeconomics work here.

Along with ESCoE and Rebuilding Macroecocomics we were also delighted to take part in this year's Royal Economic Society Annual Conference

New Occasional Paper

In October, after a break of 15 years (!), we launched NIESR Occasional Paper no 58 "Renewing our Monetary Vows - Open Letters to the Governor of the Bank of England" (edited by Jagjit Chadha and Richard Barwell). The paper proposes a series of reforms that the Chancellor and the next Governor of the Bank should consider. You can download the paper here or buy a bound paper copy for �10 (+�1.50 p&p)

Stay Updated!

Don't forget, you can sign up to receive our latest updates on GDP, CPI, Wages, DIscussion Papers and this quarterly Newsletter (tell your friends!)

Tick the relevant boxes here

Find out about Corporate Membership

Copyright � 2019 National Institute of Economic and Social Research. All rights reserved.

Want to change how you receive these emails?

You can update your preferences or unsubscribe from this list.

National Institute of Economic and Social Research�s Wage Tracker

Figure 1 � Average weekly earnings growth (per cent per annum)

1 �

Average weekly earnings growth (per cent per annum

Main points

According to new ONS statistics published this morning, UK average weekly earnings (AWE) expanded by 3.5 per cent excluding bonuses in the three months to October compared to the year before (figure 1).

Total earnings growth including bonuses was 3.2 per cent over the same period, with the drop relative to the previous quarter being explained by higher than usual bonus payments in October 2018 but normal

bonus contributions in the same month this year.

With CPI inflation at 1.6 per cent in the three months to October, real wages grew at an annual rate of 1.8 per cent over the same period excluding bonus payments (1.5 per cent including bonuses).

The Wage Tracker indicates that nominal earnings growth excluding bonuses will have been around 3� per cent in the fourth quarter of 2019, and just above 3 per cent if bonus payments are taken into account.

Based on NIESR Wage Tracker and GDP Tracker information, we estimate unit labour cost growth picked up to more than 3� per cent per annum in the fourth quarter, higher than what new ONS estimates

suggest unit labour cost growth has been for the last two years.

Dr Arno Hantzsche, Principal Economist in Macroeconomic Modelling and Forecasting, said:�Earnings growth has softened slightly in recent months. With the general election removing some of the political uncertainty, there is a chance for a renewed pick-up in pay dynamics as we enter

the new year. But with real wage growth outpacing productivity improvements and unit labour cost growth elevated, such a pick-up would unlikely be sustained.�

______________________________________________________________________

This email has been scanned by the Symantec Email Security.cloud service.

For more information please visit http://www.symanteccloud.com

______________________________________________________________________

National Institute of Economic and Social Research�s

GDPTracker

Figure 1 -

UK GDP growth (3 months on previous 3 months, per cent)

Main points

�The UK economy is on course to post zero growth in the fourth quarter of 2019, consistent with growth of 1.4 per cent in 2019 as a whole. On the basis of recent trends we tentatively

forecast service sector-driven growth of 0.3 per cent in the first quarter of 2020 (figure 1).

�According to new ONS statistics published this morning, the UK economy grew by 0.1 per cent in the three months to November, a little faster than we had expected last month reflecting

upward revisions to the September and October data.

�Output fell by 0.3 per cent in November itself, with falls of 0.3 per cent in services and 1.7 per cent in production outweighing an increase of 1.9 per cent in construction. Monthly

data is volatile and the forecast improvement in growth in the first quarter of 2020 assumes that the weakness in services in November proves to be temporary.

�Recent surveys suggest that economic activity was little changed in December, though there is some evidence of an improvement in business sentiment after the election.

Dr Garry Young, Director of Macroeconomic Modelling and Forecasting, said:�The latest data confirm that economic growth in the United Kingdom had petered out at the end of last year. GDP was virtually flat in the three months to November

and the latest surveys point to further stagnation in December. While there is some evidence of an improvement in business optimism following the general election, it is doubtful that this will

do much to change the short-term economic outlook of further lacklustre growth.�

Please find the full analysis in the document attached

For more information please contact Phil Thornton on

p.thornton@niesr.ac.uk / 0207 654 1982 or Luca Pieri on

l.pieri@niesr.ac.uk/ 079 305 44631

Kind Regards,

The Comms Team

----------------------------------

Check out our General Election 2019 Analysis

The National Institute of Economic and Social Research is a company registered in England and Wales (company number 00341010) and a charity registered

in England and Wales (charity registration number 306083).

This email and any attachments are confidential and intended for the addressee only. If you are not the intended recipient you must take no action based on them, nor must you copy or show them to anyone. Please contact the sender if you believe you have received

this email in error.

We have taken reasonable precautions to ensure this communication does not contain viruses. We cannot accept liability for any damage

your system sustains due to software viruses. You should carry out your own information security and virus checks before opening any attachments or following any links. The contents of this email may be intercepted, monitored and/or recorded by a third party.

We exclude any liability arising from any interception.

______________________________________________________________________

This email has been scanned by the Symantec Email Security.cloud service.

For more information please visit http://www.symanteccloud.com

______________________________________________________________________

National Institute of Economic and Social Research�s Wage Tracker

Figure 1 � Average weekly earnings growth (per cent per annum)

1 �

Average weekly earnings growth (per cent per annum

Main points

According to new ONS statistics published this morning, UK average weekly earnings (AWE) expanded by 3.4 per cent excluding bonuses in the three months to November compared to the year before,

and by 3.2 per cent if bonus payments are taken into account (figure 1).

Earnings growth in the public sector was in line with forecasts published in our Wage Tracker one month ago while private sector outturns were again marginally weaker than forecast.

With CPI inflation at 1.6 per cent in the three months to November, real wages grew at an annual rate of 1.8 per cent over the same period excluding bonus payments (1.6 per cent including

bonuses).

The Wage Tracker indicates that nominal earnings growth excluding bonuses will have been 3.3 per cent in the fourth quarter of 2019 and is expected to remain around 3� per cent in the first

quarter of 2020.

Based on NIESR Wage Tracker and GDP Tracker information, we estimate unit labour cost growth eased to around 3 per cent per annum in the fourth quarter and is expected to

stay at this rate in the first quarter of 2020.

Dr Arno Hantzsche, Principal Economist in Macroeconomic Modelling and Forecasting, said: �As expected, earnings growth continued to soften

a little towards the end of last year but employees should see 2020 start with stronger real pay growth as demand for workers is holding up, inflation eases and upratings in the National Living Wage and minimum wages will benefit those on low incomes.�

______________________________________________________________________

This email has been scanned by the Symantec Email Security.cloud service.

For more information please visit http://www.symanteccloud.com

______________________________________________________________________

National Institute of Economic and Social Research�s

GDPTracker

Figure 1 -

UK GDP growth (3 months on previous 3 months, per cent)

Main points

�Latest economic data confirms that the UK economy posted zero growth in the fourth quarter of 2019, consistent with annual growth of 1.4 per cent in 2019.

We expect a service sector-driven growth of 0.2 per cent in the first quarter of 2020, marginally revised from our forecast last month (figure 1).

�Data published this morning by the ONS suggest that the UK economy grew by 0.0 per cent in the three months to December, consistent with what we had forecast

last month.

�Output increased by 0.3 per cent in December itself, largely reflecting growth in the services sector.

�Recent surveys show that all major sectors recorded an improvement in performance in January, primarily due to receding political uncertainty.

Dr Kemar Whyte, Senior Economist, said:�The UK is benefitting from a post-election boost to business and consumer confidence,

latest survey evidence confirms. However, there is no guarantee that this will be sustained. The latest data confirm that economic growth in the United Kingdom had stagnated at the end of 2019. Despite the post-election bounce to confidence, the potential

complexity of trade negotiations with the EU means a high degree of uncertainty could resurface, which would weigh heavily on economic growth.�

Please find the full analysis in the document attached

For more information please contact Phil Thornton on

p.thornton@niesr.ac.uk / 0207 654 1954 or Luca Pieri on

l.pieri@niesr.ac.uk/ 079 305 44631

Kind Regards,

The Comms Team

----------------------------------

Check out our General Election 2019 Analysis

The National Institute of Economic and Social Research is a company registered in England and Wales (company number 00341010) and a charity registered

in England and Wales (charity registration number 306083).

This email and any attachments are confidential and intended for the addressee only. If you are not the intended recipient you must take no action based on them, nor must you copy or show them to anyone. Please contact the sender if you believe you have received

this email in error.

We have taken reasonable precautions to ensure this communication does not contain viruses. We cannot accept liability for any damage

your system sustains due to software viruses. You should carry out your own information security and virus checks before opening any attachments or following any links. The contents of this email may be intercepted, monitored and/or recorded by a third party.

We exclude any liability arising from any interception.

______________________________________________________________________

This email has been scanned by the Symantec Email Security.cloud service.

For more information please visit http://www.symanteccloud.com

______________________________________________________________________

National Institute of Economic and Social Research’s Wage Tracker

According to new ONS statistics published this morning, UK average weekly earnings (AWE) expanded by 3.2 per cent excluding bonuses

in the three months to December 2019 compared to the year before, and by 2.9 per cent if bonus payments are taken into account (figure 1).

Earnings growth in the public sector was in line with forecasts published in our Wage Tracker one month ago while private sector

outturns were slightly weaker than forecast, mainly because of smaller bonus payments in December last year.

With CPI inflation at 1.4 per cent in the three months to December, real wages grew at an annual rate of 1.8 per cent over the

same period excluding bonus payments (1.4 per cent including bonuses).

The Wage Tracker indicates that nominal earnings growth excluding bonuses will be 3� per cent in the first quarter of 2020 and

just above 3 per cent including bonuses.

Based on NIESR Wage Tracker and GDP Tracker information, we estimate unit labour cost growth eased to around 3 per cent per annum

in the fourth quarter and is expected to stay at this rate in the first quarter of 2020.

“The recent slowdown in earnings growth is expected to be temporary as there is little slack in the labour market and the number of vacancies ticked up. Real average weekly earnings

are only back to their 2008 levels, which illustrates the long-lasting impact of the financial crisis on the average British worker. Cyrille Lenoel, Senior Economist in Macroeconomic Modelling and Forecasting

For further information please contact

Phil Thornton or Sarah Stevens

on 020 7222 7665 / 0207 654 1954p.thornton@niesr.ac.uk /

s.stevens@niesr.ac.uk

National Institute of Economic and Social Research

2 Dean Trench Street

Smith Square

London, SW1P 3HE

United Kingdom

Switchboard Telephone Number: 020 7222 7665

Website:

http://www.niesr.ac.uk

The National Institute of Economic and Social Research is a company registered in England and Wales (company number

00341010) and a charity registered in England and Wales (charity registration number 306083).

This email and any attachments are confidential and intended for the addressee only. If you are not the intended recipient you must take no action based on them, nor must you copy or show them to anyone. Please contact the sender if you believe you have received

this email in error.

We have taken reasonable precautions to ensure this communication does not contain viruses. We cannot

accept liability for any damage your system sustains due to software viruses. You should carry out your own information security and virus checks before opening any attachments or following any links. The contents of this email may be intercepted, monitored

and/or recorded by a third party. We exclude any liability arising from any interception.

______________________________________________________________________

This email has been scanned by the Symantec Email Security.cloud service.

For more information please visit http://www.symanteccloud.com

______________________________________________________________________

NIESR May 2020 Newsletter

View this email in your browser

National Institute of Economic and Social Research

Newsletter - May 2020

Welcome to NIESR's newsletter, a regular catch-up with our activities and preview of the coming weeks.

NIESR has followed government advice regarding the global pandemic. We are all working from home. Other than that, it''s business as usual! Authoritative and independent analysis has never been more needed than now - and we''re here to help. Please get in touch if we can work together in any way.

Our excellent networks, state of the art modelling, cross-disciplinary research and economic measurement makes NIESR ideally placed to lead debate on the social and economic impact of the Coronavirus. We have started to publish a range of perspective from our staff and partners, and will continue to do so over the coming weeks. We have collated the research on our website here, and will continue to update this page.

May 2020 GDP, Wage and CPI Trackers Out Now

This month, our GDP Tracker found that the economy is contracting at a rapid pace. The ONS preliminary estimates suggest that growth declined by 2.0 per cent in the first quarter of 2020, broadly consistent with what we suggested it could be last month. In light of the preliminary release, we forecast growth in the second quarter to decline sharply by about 25 to 30 per cent. Read more here.

OurWage Trackerthis monthlooks at the first signs of the severe labour market impact of COVID-19. Official labour market statistics are mainly lagging indicators and are only just beginning to show the impact of COVID-19. By early May a quarter of paid employees had been furloughed, with 80 per cent of their pay (up to ?2,500 per month) being met by the government. This will mean that measured average earnings will fall in the short term, reflecting the lower pay of those who have been furloughed. Read more here.

Our May CPI Trackerfound that underlying inflation increased by 0.3 percentage points to 1 per cent in the year to April 2020, as measured by the trimmed mean, which excludes 5 per cent of the highest and lowest price changes. The historical relationship between current trimmed mean inflation and future CPI inflation implies CPI inflation of 2.1 per cent in the year to April 2021. Read more here.

Our trackers are an invaluable tool during these uncertain times. We acknowledge that forecasting is subject to errors, and so is a hazardous exercise. However, that does not by itself invalidate the exercise because both the producers and consumers of forecasts understand that errors will occur. Forecasting allows us to think about possible futures and plan accordingly.

New Projects

Potential Destitution and Foodbank Demand Resulting from COVID-19 Crisis In UK

We are assisting the Trussell Trust(Britain's largest provider of foodbanks) by conducting a short term piece of research to address key questions about the potential impact of the COVID-19 emergency on destitution and the demand for foodbank services across the UK in the coming weeks and months. Craig Thamotheram, Senior Economist at NIESR, is the project leader.

Modelling the Impact of the Coronavirus Pandemic on the UK economy

Funded by ESRC, and partnering with BEIS and the Cabinet Office, this projectseeks to use and develop NIESR's modelling capability to estimate the short- term impact of the coronavirus pandemic on the UK economy, and to assess longer-term issues on how the economic recovery is affected by different policy measures. Garry Young, Deputy Director of NIESR, is the project leader.

Estimating Food and Drink Demand Elasticities

Funded by the Department for Environment, Food and Rural Affairs, this project is about estimating demand elasticities for food and drink which allow us to understand both the short-term and long-term consumer responses to changes in prices and income, including from different socio-economic groups.

This project is with colleagues at NIESR (Ana Rincon-Aznar, Larissa Marioni and Elena Lisauskaite) and with colleagues at Birkbeck (Sandeep Kapur, Ron Smith & Walter Berkert).

IAA Grant

In a second tranche of funding from the Economic and Social Research Council, we have received supplementary funding under their Impact Acceleration Award scheme. This will allow us to apply NIESR research to a wide range of Coronavirus policy debates over the next six months. If you would like to hear more about how you can partner with NIESR, whether through the IAA or otherwise, please do get in touch.

New Partnership with the University of Glasgow

On Tuesday 12 May we held a joint webinar with the University of Glasgow: "Covid Crisis: What Next for The UK and World Economy?" where NIESR Director Jagjit Chadha outlined the prospects for the UK and world economy in light of the Covid-19 crisis Sir Anton Muscatelli chaired the session.

The event was part of a much bigger collaboration which is developing between NIESR and the University of Glasgow. As a starting point, we will together apply NIESR''s internationally renowned forecasting and modelling expertise to Scotland, and the University will become a partner in NIESR''s UK and global forecast. The Institute has also offered to host students on the University of Glasgow''s new masters course in Data Analytics in Finance for their project work, and we are exploring possible joint appointments.

National Institute Economic Review Issue 252 Out Now

The May edition of the National Institue Economic Review focuses on new research exploring the rise of Global Value Chains (GVCs). It is becoming clear that the economic and social consequences of the current pandemic will be profound and long-lasting, and still largely uncertain, and highlight the extent to which the economic crisis is transmitted not only through domestic policies but also through severe disruption to trade in global supply chains. This undoubtedly implies widespread changes to the way in which countries and firms will trade in future decades, which will recognise the globalised scope of shocks.

In the NIESR May Review, Leading experts in the field provide in-depth analysis of various aspects of this major issue in world trade. The articles cover a wide range of topics, from protectionism, to the impact from COVID-19 and Brexit, the declining EU share in global manufacturing, as well as other key trends affecting UK and European industries. For a limited time only, the review is not behind a paywall andis available to read for free here.

Subscribe to the National Institute Economic Review

NIESR in the Media

NIESR Director Jagjit Chadha was interviewed on BBC Radio 4 on 19 May 2020 to discuss the latest unemployment figures. You can listen here.

NIESR Director Jagjit Chadha was interviewed on BBC Radio 5 Live on 19 May 2020 to discuss the latest economic figures and the unemployment statistics. You can listen here (from 21 mins).

Garry Young, Deputy Director of NIESR was interviewed on LBC Radio on 19 May 2020 to discuss the latest unemployment figures. You can listen here

"Why Covid-19 should change the conversation on migrant workers" in the New Statesmen by Andrew Aitken, Senior Economist at NIESR, and Chiara Manzoni, Senior Social Researcher at NIESR (18 May 2020)

Garry Young, Deputy Director of NIESR was interviewed on BBC Radio 4 on 14 May 2020 to discuss the ONS GDP data and our GDP Tracker. You can listen here.

"How bad is the economic damage looking-and what are the prospects for recovery?" in Prospect Magazine by Jagjit Chadha, NIESR Director (13 May 2020)

NIESR Director Jagjit Chadha was one of the contributors in BBC Radio 4''s The Briefing Room episode "Coronavirus and the economy" (from approx 17mins in) that took place on 9 May 2020

NIESR Alumni

Are you a former employee, intern or fellow of NIESR? Want to stay in touch? Join our Alumni Mailing List to receive invites and content from NIESR. By signing up, you will become part of a vast alumni network of economists and social researchers across the UK & abroad.

SIGN UP HERE

Copyright ? 2020 NIESR, All rights reserved.

You can update your preferences or unsubscribe from this list

National Institute of Economic and Social Research's

GDPTracker

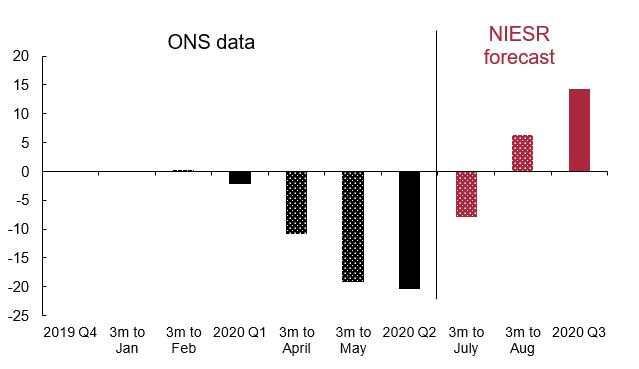

GDP could contract by 15 to 25 per cent in second quarter

Figure 1 -

UK GDP growth (3 months on previous 3 months, per cent)

Note: Grey and Burgundy bars show high and low scenarios

Main points

Once in a century event poses major threat to UK growth. The UK economy could now see growth decline by 5% in